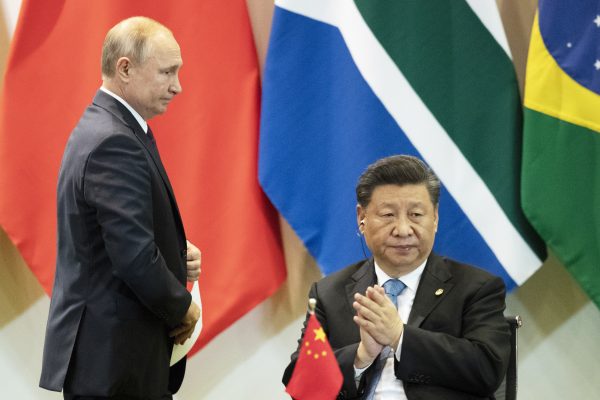

China’s President Xi Jinping, proper, and Russia’s President Vladimir Putin attend a gathering with members of the Enterprise Council and administration of the New Improvement Financial institution through the BRICS rising economies on the Itamaraty palace in Brasilia, Brazil, Thursday, Nov. 14, 2019.

Credit score: AP Photograph/Pavel Golovkin

Russia’s economic system made out higher than anticipated through the disaster final 12 months. Mixture GDP solely dropped within the vary of three.5-4 % regardless of worse forecasts. The Kremlin made do with comparatively restricted disaster spending measures, betting on China and different economies to get well rapidly sufficient to isolate the financial injury as a substitute. Though oil and pure fuel – nonetheless Russia’s main exports – took a shellacking till the previous couple of months of the 12 months, Moscow lucked out: A broad vary of non-oil and fuel commodities together with gold entered a bull market by summer time, aided by a $500 billion fiscal stimulus package deal in Might from China.

China’s spending was geared towards funding and companies, a lot of which produce items for export or construct houses and infrastructure. Whereas economies the world over together with Russia struggled with a number of waves of infections, lockdowns, and constraints on providers demand, China’s exports of products surged to file ranges by December – a surplus of $78 billion in December alone. Mockingly, it was the under-development of small and medium-sized companies and providers within the Russian economic system that spared the Russian policymakers a a lot steeper price ticket in stimulus spending.

The excellent news, nevertheless, stops there.

For the previous decade, China has achieved greater than another economic system to maintain Russia’s oil export earnings and thus its financial mannequin – China alone accounted for simply over half of the expansion of worldwide oil demand between 2008 and 2019. China’s client restoration has lagged behind that of its industrial restoration from the worst of the disaster, and whereas the economic system is lastly approaching steadiness, it’s nonetheless locked right into a structurally slowing development price.

Refining large Sinopec is now forecasting China’s petroleum product demand to peak by 2025 due to the affect of coronavirus and accelerated adoption of electrical autos. Nobody is for certain of what comes subsequent for power markets, however one factor is evident: This shock is nothing just like the International Monetary Disaster and the percentages of a longer-run return to excessive oil costs are slim at greatest. The Kremlin has exhausted Russia’s development potential with its present financial construction. As China’s function underpinning power demand and the composition of its development change post-COVID-19, Moscow must grapple with its home coverage failures.

Provide-Siders of the World, Unite!

Any substantial financial restoration in Russia requires increased oil costs, realistically within the vary of $60-65 a barrel, in an effort to generate a mixture of extra funds revenues and better intermediate demand for items and providers to maintain the stagnant sort of development seen in 2018-2019. Oil is at the moment above $50 a barrel, however considerations about Europe’s vaccine rollout woes and extra infectious strains of COVID-19 are weighing down any constructive outlook. Russia’s provide aspect administration of the oil market inside OPEC+ helped stabilize the oil market, however exacerbates the issues created by collaborating in manufacturing cuts. They’ve develop into a necessity to handle funds deficits, the ruble change price, and the well being of the nation’s forex reserves and banking sector by pushing up costs. However the cuts cut back home demand for items and providers, spilling over into different sectors together with manufacturing, which skilled its first internet contraction since 2009 final 12 months. Making certain oil worth stability by paring again output finally ends up squeezing development as a result of it suppresses home demand.

Russia’s commerce surplus displays its dependence on exterior demand for its most important useful resource exports to drive development and its enterprise cycle. What’s fascinating is that simply as oil and fuel costs started the gradual means of stabilization in Might to June, Russia went from surplus to a commerce deficit with China. The deficit then widened, reaching $5.5 billion for the month of November. Evidently China’s exporter-centric stimulus pushed extra manufacturing into Russia, doubtless aided by a greater change price than the euro towards the ruble. However a deficit within the longer run is an issue for Moscow. The difficulty stems from what Russia’s making an attempt to export extra of, the way it impacts its home economic system, and the way bilateral commerce interacts with Russia’s power export dependence.

Gone Agro

Usually a bilateral commerce deficit is irrelevant. Nations’ commerce balances mirror how a lot they produce versus how a lot they devour and no matter extra or deficit they’ve with one nation will get distributed with others. However in Russia’s case, a commerce deficit with China displays a post-Crimea shift: European firms in addition to Asian corporations with provide chains in China moved to seize market share or relocate manufacturing from Europe after the ruble devalued in 2014-2015, the West utilized sanctions, and Russia then utilized counter-sanctions on agricultural imports from Europe. Deficits with China are tougher to make up elsewhere as Europe’s extended recession and environmental insurance policies are accelerating the destruction of demand for Russia’s power exports longer-term. Meaning extra agricultural exports – certainly one of Russia’s few areas of aggressive benefit – are wanted to revive extra steadiness for commerce with China.

However there’s an issue with agricultural exports in the meanwhile. Wheat costs shot up final 12 months as extra meals was consumed at residence, file summer time warmth affected harvests, and Russian export quotas squeezed worldwide costs. Russia is the world’s largest wheat exporter and noticed a harvest of 132.9 million tons final 12 months, a 9.7 % improve over 2019. Regardless of the excessive manufacturing ranges, costs for primary items like bread and pasta started to rise considerably towards the top of 2020 due to the affect of export costs on the charges producers quoted domestically.

This was politically delicate. Rising costs have decreased disposable incomes by almost 5 %. Russia’s response has been to impose stricter export quotas, increased tariffs on wheat exports, and to set worth controls. All of those are more likely to worsen shortages whereas making an attempt to drive commerce companions to eat worth will increase and take in inflation that might in any other case be occurring in Russia domestically. That doesn’t encourage confidence for Chinese language policymakers to increase Russia’s market entry on the similar time they’re enhancing it slowly for Central Asia’s meals exporters. Whilst Russia expands agricultural exports to China, it’s unclear they’ll have the ability to offset what might develop into a constant, if small, commerce deficit.

Reaching Maturity

Beijing faces a number of challenges at residence in making an attempt to protect a sustainable restoration after the COVID disaster passes. Fears that an actual property bubble collapse might contract GDP by as a lot as 5 to 10 % prompted curbs on financial institution loans for property, more likely to decelerate development within the 12 months forward. Extra state corporations are being allowed to default, deflating some dangers within the monetary sector but in addition worrying some traders. Newer lockdowns are additionally more likely to damage client spending, nonetheless weaker than it must be. Whereas China plowed forward in 2020 and lifted the Russian economic system, that dynamic is altering in 2021. Slower development lies forward.

China’s financial maturation right into a client economic system is a intestine punch to Russia’s financial mannequin. With out robust exterior demand development for oil and fuel, Russians face a decline of their requirements of residing as state coverage refuses to stimulate home demand whereas defending giant sectors from commerce competitors. Sino-Russian relations are gone the purpose of needing symbols of shut ties. Comply with the cash. Most Chinese language traders stay skeptical of Russian investments, most joint initiatives are politicized, and commerce remains to be tightly managed. China beneficial properties much more from the established order than Russia.

Nicholas Trickett is an analyst overlaying oil and fuel markets, commerce and political economic system, with a concentrate on Russia and the post-Soviet house.. He holds an MA in Russia/Eurasia research from the European College on St. Petersburg and an MSc in worldwide political economic system from LSE. He writes a day by day publication overlaying the political economic system and geopolitics of COVID-19 and the power transition in Russia and Eurasia known as OGs and OFZs.

{kind=link}